A significant discussion to reevaluate Ethereum’s token issuance model has stirred debate over the future of ETH staking economics.

As Ethereum sees an upward trend in ETH staking, projections suggest this could lead to a majority of ETH being locked in staking contracts, prompting concerns over the network’s future dynamics. In response, Ethereum Foundation researchers Ansgar Dietrichs and Caspar Schwarz-Schilling have introduced a proposal to tweak Ethereum’s issuance policy to maintain a balanced staking ratio, aiming to prevent potential negative effects such as inflationary pressures on non-stakers and centralization risks.

However, this solution has sparked a contentious debate within the Ethereum community, with some members voicing strong opposition against altering the monetary policy in a way they believe could undermine Ethereum’s foundational principles and its appeal to institutional investors.

As James Spediacci tweeted, “It almost seems like a coordinated attack on Ethereum that a few people are suggesting adjusting the ETH issuance curve again and changing the monetary policy when the SEC currently has Ethereum under a microscope.”

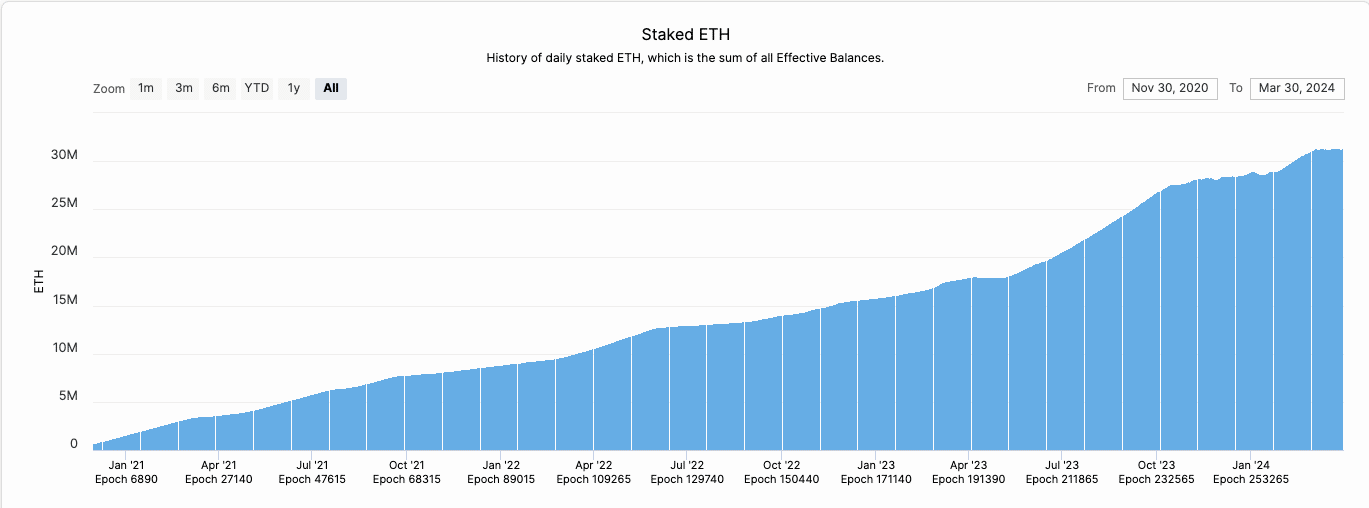

The Amount of Staked ETH Has Been on the Rise

Since Ethereum’s transition from Proof of Work to Proof of Stake 18 months ago, known as “The Merge,” the dynamics of ETH staking have shifted dramatically. Currently, about 31 million ETH, roughly 26% of the total supply, are staked. This figure has been on an upward trajectory, from 11% at the time of the Merge and 15% at the time of the Shapella upgrade, which enabled the withdrawal of staked ETH from the Beacon Chain in April 2023.

There are several drivers behind the progressive increase in staking, including the overall improvement in the network’s security and stability, innovations like liquid staking providers that lower the barrier to entry for staking, and the enticement of additional rewards. Notably, these additional rewards include those from Maximal Extractable Value (MEV), as well as opportunities for airdrop farming, which add to the attractiveness of staking beyond the primary consensus layer rewards.

Staking Demand Will Continue to Increase

The staking ratio is set to increase in the upcoming months and years, as highlighted in a blog post by Mike Neuder from the Ethereum Foundation, due to five reasons:

- Appreciating ETH Price: An increasing ETH price makes staking more attractive due to higher USD-denominated yields.

- Restaking Demand: Platforms like EigenLayer are driving interest in restaked ETH, with the potential for airdrops adding to the appeal.

- Interest Rates: Lower interest rates could shift institutional capital towards staking for better yields.

- Liquid Staking Tokens (LST)/Liquid Restaking Tokens (LRT): These tokens lower the barrier to staking and are expected to attract significant capital inflows.

- Staked ETH ETFs: The possibility of Ethereum-based ETFs, which include staking in their model, could introduce a substantial new audience to staking.

Why a High Staking Ratio Might Be Bad

However, the prospect of a continually increasing staking ratio raises several concerns.

“We argue that high staking ratio regimes come with negative externalities that affect ETH holders, (solo) stakers, as well as the protocol itself,” they wrote in the proposal.

Dietrichs and Schwarz-Schilling’s analysis points out potential issues with nearly all ETH being staked, particularly with a significant portion being locked in LSTs such as Lido’s stETH, Coinbase’s cbETH, or Rocket Pool’s rETH. According to the authors, a scenario where the staking ratio approaches 100% is troubling for several reasons:

- Real staking yield will diminish: As the staking rate approaches 100%, real yields from staking could drop to zero. Although rewards from the protocol continue, the total supply of ETH increases at the same rate, effectively nullifying real gains for stakers.

- ETH will become “expensive” money: High staking rates could make holding ETH costly due to increased inflationary pressure on non-stakers. When lots of ETH is staked, people who don’t stake see the amount of their ETH decrease proportionally compared to those who do stake. This could undermine ETH’s role as a cost-effective and trustless asset on the Ethereum network.

- Threat to ETH’s status as default currency: The expensive nature of holding ETH might challenge its position as the default currency of Ethereum, leading to friction in transactions and a shift towards alternative tokens or protocols. People might start using other tokens that give them rewards, like Lido’s stETH, for daily use. This means ETH might not be the main currency people use on Ethereum anymore.

- Risk of centralization and “too big to fail” entities: A few dominant staking tokens like Lido, which currently has 30% of all staked ETH, could amass excessive influence over Ethereum’s underlying protocol, posing risks to the network’s decentralization and governance. So, if there’s a smart contract vulnerability in Lido’s cost, and they represent the majority of the network, in theory, they could fork the chain to avoid their losses.

The Proposal

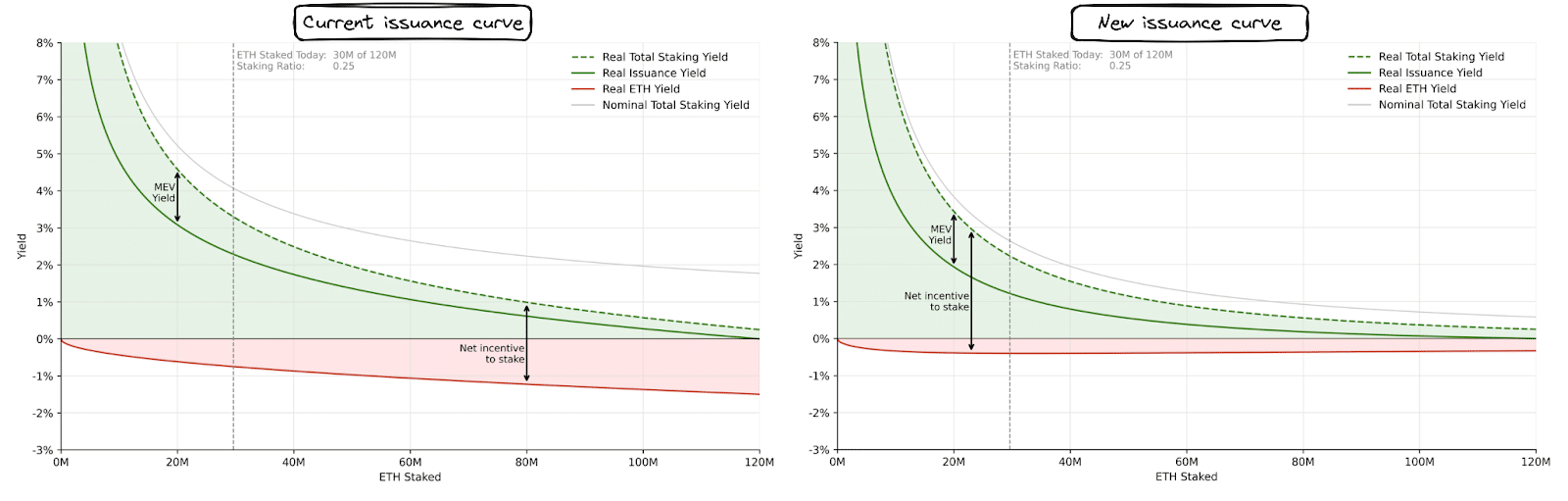

To mitigate these risks, on February 21, Ansgar and Caspar proposed a recalibration of Ethereum’s issuance curve, which involves a shift towards Stake Ratio Targeting, a nuanced approach that aims for a balanced staking ratio instead of a fixed quantity of staked ETH.

The proposed change aims to decrease the incentive for new staking inflows by introducing a revised formula for calculating staking rewards. The current issuance curve, defined by a parameterized inverse square root function, doesn’t cap rewards in a way that prevents an excessive total staking ratio.

The new formula intends to address this by adjusting rewards to discourage staking beyond a certain threshold, thus aiming to stabilize the staking ratio and ensure network security without inviting negative externalities. While the curve might not need to turn negative abruptly to be effective, a gradual approach towards zero rewards past a certain staking level could suffice to target a suitable staking range. For example, under the current issuance curve, at 80 million ETH staked, the nominal yield would be 2%, whereas under a possible revised curve, the same amount of ETH staked could yield 1%.

Nevertheless, the authors don’t explicitly say what the ideal staking ratio should be. “It is inherently hard to objectively reason about it and needs to be discussed more broadly in the community,” they wrote.

Dietrichs and Schwarz-Schilling’s proposal, premised on the assumptions that most ETH will eventually be staked, predominantly through Liquid Staking Tokens (LSTs) and Liquid Restaking Tokens (LRTs), is fundamentally about steering the network towards an inevitable future under controlled terms. They argue that as staking becomes increasingly prevalent, the staking rewards will naturally diminish under the current issuance curve.

By proposing a change in the issuance curve now, while the staking ratio is still relatively low, they aim to adjust the incentives in a way that preempts the potential negative outcomes of an excessively high staking ratio. This proactive approach seeks to maintain the balance and health of the Ethereum ecosystem by ensuring that the transition towards higher staking ratios does not compromise the network’s security, dilute ETH holders unnecessarily, or disadvantage solo stakers.

Negative Community Reaction

While the Ethereum Foundation researchers intended to initiate a discussion, the community was up in arms, with the majority signaling that this was not a good idea for Ethereum to pursue.

Eric.eth, a co-author of one of Ethereum’s most important improvement proposals (EIP-1559), is against changing the curve. “Seeing some growing discussion from researchers and others in the community about tweaking the PoS issuance curve. The general disregard for how hard we’ve worked for a decade establishing ETH being money is concerning. I’ll fight this idea with anything I have,” he wrote on X.

His comments echo some critics who say that frequent changes in monetary policy erode confidence among users and investors, distancing Ethereum from the “hard money” characteristic and “credible neutrality” that underpin its value proposition, in contrast to the perceived stability of Bitcoin.

Gnosis co-founder Martin Köppelmann pointed out that changing the issuance curve “does not fundamentally improve Ethereum – it just shifts incentives from one group to another,” while Jon Charbonneau, founder of DBA, said that “these tweaks try to solve an unsolvable problem of fundamental tradeoffs in PoS.”

Additionally, altering the issuance curve could dilute Ethereum’s attractiveness as a yield-generating asset for ETFs and institutional investors whose interest in Ethereum is based on its existing “yield” narrative. Similarly, projects built on Ethereum might suffer due to the shift in expectations around monetary policy stability.

Regulatory Risks?

Another community member pointed out that, in the midst of the Securities and Exchange Commission investigation of the EF, this move is not smart, as it would imply that the Foundation indeed runs managerial efforts over Ethereum. This is significant because it is one of the prongs of the Howey Test, and the SEC could use it to argue that ETH is a security.

I love and respect EF researchers.

We would not be where we are without their precious work and they'll keep on being very valuable.

But goddamnit, sometimes, they can't read the room! pic.twitter.com/Lcau6VWpAE

— Jrag.eth (@Jrag0x) April 1, 2024

Debate to Continue?

Researcher Emmanuel Awoski criticized those who wouldn’t even engage in a conversation about the issuance curve. He wrote, “Today is a good day to start calling out the trend of anti-intellectualism that’s slowly permeating the discourse around the issuance curve change. Not only are memes like this distasteful, they also represent how low we’ve fallen as a community. Now, EF researchers are getting mocked by people who haven’t spent their days/nights obsessing about solving hard problems. People whose sole contribution to crypto has been ‘I’ll pour money into some protocol and wait for the numbers to go up’.”

But negative sentiment has so far seemed to prevail. Ryan Berckmans countered saying that “it’s not anti intellectualism to point out (in meme form or otherwise) that for all its laudable technical rigor, the issuance modification proposal fails to demonstrate an understanding of basic key facets of the change management environment.”

Update, Monday, April 3, 04:15 pm ET: An earlier version of this article mistakenly displayed the name of Caspar Schwarz-Schilling as Caspar Schwarz. Unchained regrets the error.