In August of 2023, Coinbase, the top US cryptocurrency exchange, officially launched Base, its own Ethereum Layer 2 blockchain network. Built on the OP Stack, Base has seen a surge in activity in recent months, including a whopping 3,200% increase in daily new users after the Ethereum Dencum upgrade, and the rise of buzzworthy projects on the protocol such as social networking application Friend.tech and the decentralized social network Farcaster.

Since becoming a publicly traded company in April of 2021, Coinbase’s stock performance has often been correlated with crypto price fluctuations and major industry news. Coinbase reports its first-quarter earnings on Thursday, May 2, and its shares are up 31% year to date and a whopping 354% over the past year as crypto prices have soared. It closed trading on Friday at $236.32.

As detailed in a February letter to its shareholders, part of the exchange’s plans for growth includes looking beyond trading-related revenue and “driving utility in crypto with experiments in payments using USDC and Base.”

Read more: 3 Reasons Why Layer 2 Network Base Has More Than Doubled Its Total Value Locked This Year

Speaking recently with Laura Shin on the Unchained podcast, Reflexivity Research co-founder Will Clemente said “the Street isn’t really pricing in the crypto native revenue that I think a lot of the crypto natives understand.”

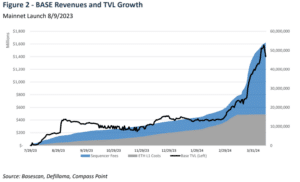

One of the types of crypto native revenue Clemente is referring to is “sequencer fees,” which are paid to the Ethereum Layer 2 entities responsible for ordering and processing transactions that are then recorded on the Ethereum mainnet. For each transaction on an L2, a small fee is paid to the “sequencer,” which in this case is Coinbase.

Clemente said that he believes the excitement around Base projects, such as the upcoming Friend.tech airdrop, coupled with the exchange’s high throughput and low fees, position the network to be the “biggest competitor to Solana.” Solan’s token, SOL, has seen a massive rebound in recent months after plunging in value following the collapse of FTX.

“Over the last 30 days, Base has done $30 million of top-line revenue for Coinbase just based on the sequencer fees, which annualizes out to like $360 million a year,” Clemente said on the podcast.

The TradFi Perspective

On the other hand, Oppenheimer and Co. senior analyst Owen Lau, who covers COIN, told Unchained that despite his belief in Base’s “huge potential,” he urges “people to look at their revenue contribution and not get too ahead of themselves before Base becomes a more material contributor.”

Lau anticipates that in 2024, Coinbase as a whole will generate roughly $5 billion in revenue, with just $100 million of that, or 2%, coming from Base.

Read more: Coinbase to Store More Customer, Corporate Balances on Base

His projections fall in line with those of other COIN analysts, as Needham senior analyst John Todaro wrote to Unchained that “our case is for $50m revenue in ’24CY and in our bull case we think $300m in revenue from Base.” Additionally, “Coinbase management has given very little color on the [profit] margin profile for this segment,” wrote Todaro.

Lau’s perspective is that “their revenue is related to some of the projects happening on the layer two. If there is hype, a new project could support higher revenue on Base, but if there’s no project or that project dies down, then the Base revenue will come down quite dramatically.”

The previously mentioned blockchain-based social platform Friend.tech experienced exactly what Lau alluded to in August of 2023, where daily inflow dropped from over $16 million to $1.6 million within the span of a month.

Beyond viral projects such as Friend.tech, Base may have more practical use cases that could have sustainable long term activity. Compass Point Research analyst Joe Flynn, who maintains a buy rating and a price target of $325 on Coinbase, wrote in an April 17 report that “Base offers a lot of optionality and potential push into payments (no fee USDC payments offered today) that investors are overlooking.”

As Base stands currently, “will shareholders pay a lot of attention to or own Coinbase because of [Base]? I think investors would like to see a more consistent revenue stream before they make the final decision,” Lau said, adding “I still think the number one driver is still Coinbase volume, not the Base volume.”

Todaro shared a similar perspective, stating that “investors are much more closely watching retail volumes, retail take rates, and the SEC case with COIN as those are significantly greater drivers for revenue and margin.”

For Lau, the success of Base is more reflective of Coinbase’s long term trajectory rather than a direct contributor to COIN performance at this point, saying “longer term, you’re going to see more and more revenue sources outside of trading, which is good for the stock.”

More specifically, Todaro wrote that “Base is a fast-growing product that has serious buy-in from the crypto native community…. It would likely spur Coinbase to launch more on-chain like products.”

Bitcoin ETF Custody Revenue

Beyond Web 3 development, Coinbase has also recently diversified its revenue streams by becoming the custodian for eight of the 11 spot Bitcoin ETFs launched earlier this year, including those issued by BlackRock, Franklin Templeton, and Grayscale.

Needham’s Todaro estimates that Coinbase will earn $167 million in revenue custodying these assets in 2024, placing both Base and custody revenues in the same ballpark as minor contributors to the company’s overall performance currently.

Looking ahead however, the analyst wrote “we expect the revenue from Base to be greater than custody which is a highly competitive business and likely will see more competition in the future from traditional banking/brokerage firms. Base chain, on the other hand, is a product we do not believe a traditional finance firm could replicate.”