July 6, 2022 / Unchained Daily / Laura Shin

Daily Bits✍️✍️✍️

- Crypto broker Voyager Digital filed for Chapter 11 bankruptcy after suffering huge losses from its exposure to 3AC.

- Nexo (disclosure: a former sponsor) announced its plans to acquire Vauld, one of the crypto lenders that halted withdrawals.

- Crypto platform Bullish dismissed several employees amid the market turmoil.

- Crypto exchange Bitstamp will start charging a fee to inactive users.

- Bitmain, a hardware mining manufacturer, started selling a new Ethereum ASIC miner today.

- Tornado Cash’s governance proposal to diversify its portfolio into ETH did not pass.

Today in Crypto Adoption…

- The Bank of England called for stricter crypto regulations.

- Virtu Financial, one of the traditional finance world’s most important market maker, is hiring a weekend crypto trader.

- Vincenzo Sospiri Racing, a racing team backed by Lamborghini, announced that it will begin using non-fungible tokens (NFTs) to certify and authenticate factory car parts.

The $$$ Corner…

- Two former executives at VCs in Asia launched a new web3 investment firm.

- Bitcoin Miner TeraWulf took a $50 million loan to invest in data center infrastructure.

What Do You Meme?

What’s Poppin’?

MakerDAO to Integrate With an American Bank

By Juan Aranovich

MakerDAO is voting on whether to provide a DAI vault worth $100 million to Huntingdon Valley Bank. MakerDAO is the organization behind the DeFi protocol Maker, which is responsible for the issuance of the stablecoin DAI.

Huntingdon Valley Bank is a 151-year-old lender based in Pennsylvania, and has $500 million in assets.

The governance proposal went live on Monday, and will be closed by Thursday. If it passes, HVB would receive a loan participation facility with a 100 million DAI debt ceiling. With these funds, HVB will seek to support the growth of both its existing businesses and new ones as well.

In exchange, the bank would post real-world assets as collateral. These assets would be a portfolio of various loans, including:

- Commercial Real Estate Loans

- Commercial & Industrial Loans

- Government Guaranteed or Affiliated Loans

- Consumer Loans

- Residential Real Estate Loans

- Capital Call Line

What’s in it for Maker? For starters, they would get yield, both fixed and variable. Second, it would help Maker diversify its portfolio. Lastly, it would mean a step further towards integration with traditional markets. This last point is significant: Maker would be enabling real-world assets to make their way into DeFi.

This proposal came just one day after another important governance proposal was passed, in which the community decided to allocate $500 million to a portfolio of treasury bills and investment grade corporate bonds.

On a related note, Celsius repaid another $40 million of its debt to Maker (this story was covered in yesterday’s newsletter). As of press time, Celsius’s liquidation price dropped to ~$2,700 per BTC.

Recommended Reads

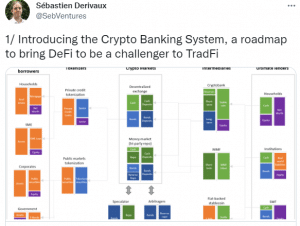

1) Sébastien Derivaux on DeFi challenging TradFi:

2) Glassnode on BTC HODLers and “Tourists”:

3) Nansen on the causes behind stETH “de-peg”:

On The Pod…

Hasu, strategic advisor to Lido, and Tarun Chitra, founder of Gauntlet, explain everything about staked ETH, aka stETH, how it should be priced, Lido’s market dominance, and much more. Show highlights:

- the role of Lido, what stETH is, and what its benefits are

- whether Ethereum’s lack of delegated proof of stake contributes to the need for stETH

- why stETH is not mispriced and why it doesn’t necessarily have to be worth 1 ETH

- the inherent risks associated with stETH

- how there was not enough liquidity to handle all the liquidations, especially in automated vaults on, for instance, Instadapp

- how automated market makers work and what Curve’s amplification factor is

- whether 3AC and Celsius had a significant impact on the stETH/ETH “de-peg”

- how does the Merge affect the liquidity of stETH

- Hasu’s and Tarun’s level of confidence that the Merge will happen this year and whether it will be a success

- what will happen to the price of stETH after the redemptions are enabled

- why Lido has achieved such a level of dominance

- how Lido decreases the cost of staking and helps improve the security of the Ethereum blockchain

- whether there is going to be a “winner take all” in the liquid staking derivatives market

- how liquidity fragmentation can cause the system to blow up

- why LDO tokenholders might not have the same incentives as ETH tokenholders

- what is the Lido’s new dual governance model and what is it trying to achieve

- whether Lido should self limit its market dominance

- how Lido coordinates validators and the role of the LDO token in this coordination

- what are the lessons to be learned from the stETH situation

- how governance is a liability to DeFi protocols

Book Update

My book, The Cryptopians: Idealism, Greed, Lies, and the Making of the First Big Cryptocurrency Craze, which is all about Ethereum and the 2017 ICO mania, is now available!

You can purchase it here: http://bit.ly/cryptopians