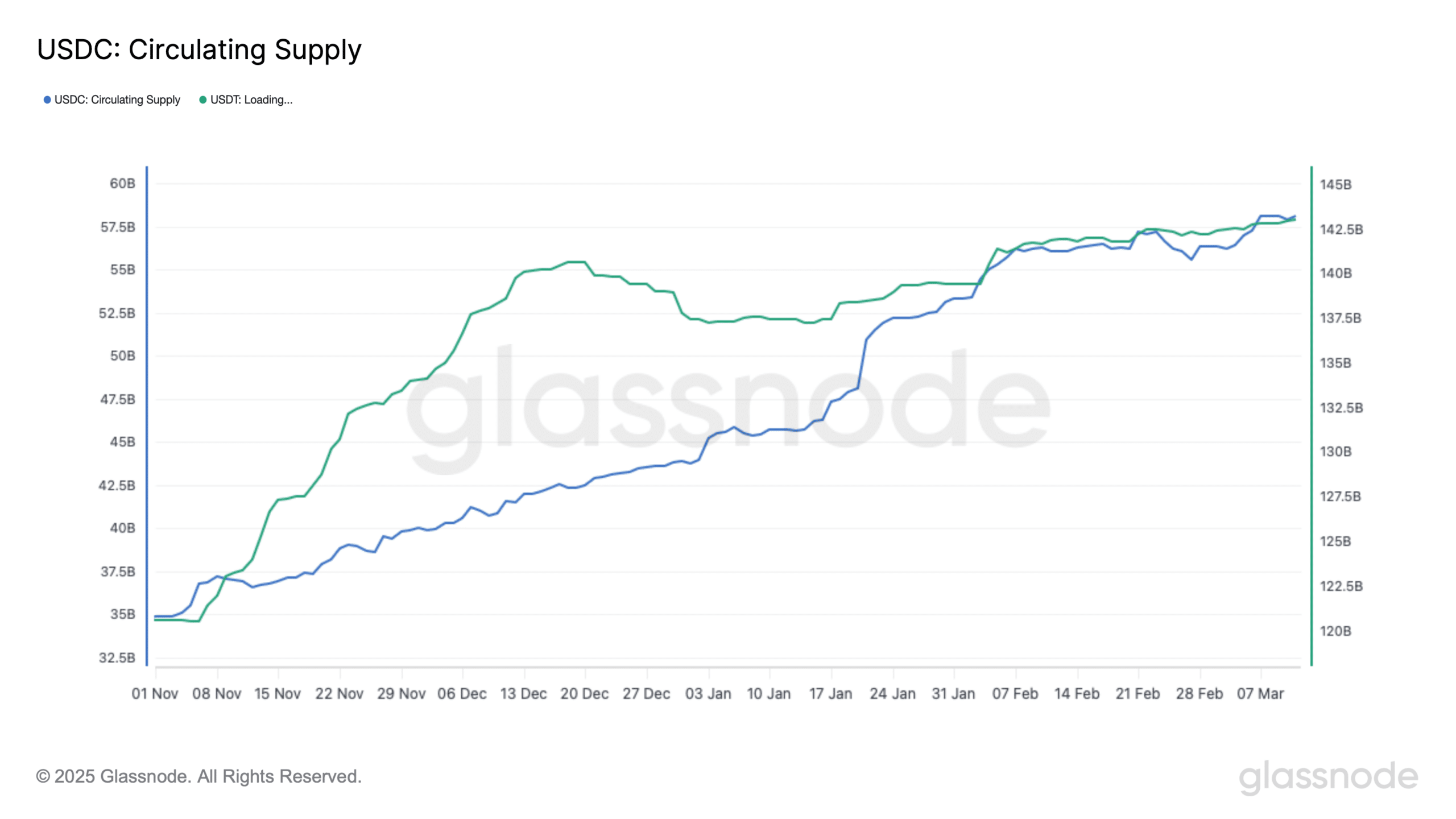

A strong argument can be made that stablecoins are crypto’s only real killer app. Led by issuing giants USDT (market cap: $143.34 billion) and USDC ($57.85 billion), the $235 billion sector is the lifeblood of the blockchain-based economy.

Stablecoins are useful in several ways. During bullish times traders track their flows into exchanges, as these assets are the dry powder necessary to start buying. They have also proven to be a critical lifeboat during stormy weather for investors that want the safety of the U.S. dollar but stay at the ready for buying opportunities.

But in this crypto market slump, traders are increasingly turning to an alternative digital asset that not only holds its value but pays a small yield.

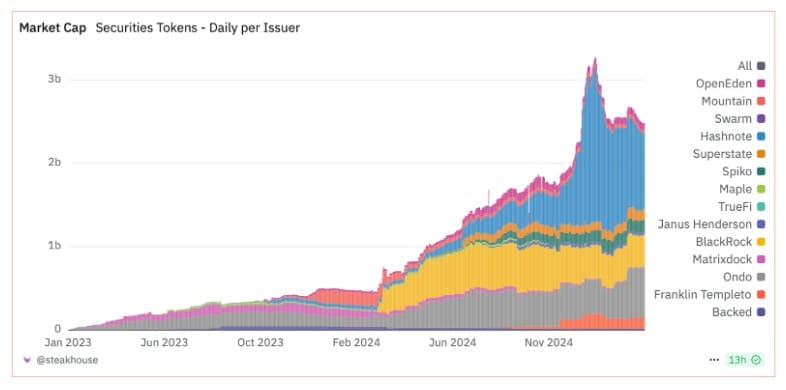

Tokenized treasuries, a subset of the growing real world asset (RWA) market that packages U.S. government debt into blockchain-based tokens, have long been the little engine that could. A year ago, in March 2024, the RWA industry trumpeted that it passed $1 billion in assets under management (AUM).

“Just happened, $1B Total Tokenized U.S. Treasuries on Public Blockchains,” tweeted industry analyst Tom Wan from Entropy Advisors.

While that number might sound big to casual observers, it is a sliver of the $28 trillion U.S. Treasury market.

One year later, the tokenized treasury market has quadrupled to approach $4 billion.

That’s still a pittance compared to the total market, but it represents 300% growth. More striking is that while there is much discussion about the growth in stablecoins in this tenuous macro environment as traders flee sinking crypto assets, tokenized treasuries have grown almost 20x as fast as their stablecoin siblings.

Stablecoins pay no interest to their holders, letting issuers like Tether and Circle invest the collateral in short-term treasuries and mint billions in risk-free profits. The product has also been in a regulatory gray zone as lawmakers in Washington, D.C. continue to make progress on legislation. It has always been a question of when traders would start demanding their share of their yield.

That appears to finally be happening.

Tokenized Treasuries Boom After Election

Stablecoins saw a big growth surge after Donald Trump was re-elected to the presidency on November 5. On that date the stablecoin market was worth $183.82 billion. Since then it added $50.95 billion, with USDT and USDC each adding more than $20 billion as traders looked to capitalize on Trump’s pro-crypto momentum that propelled the price of bitcoin to an all-time high of $108,000 in January. That amounts to a 27.71% surge for stablecoins.

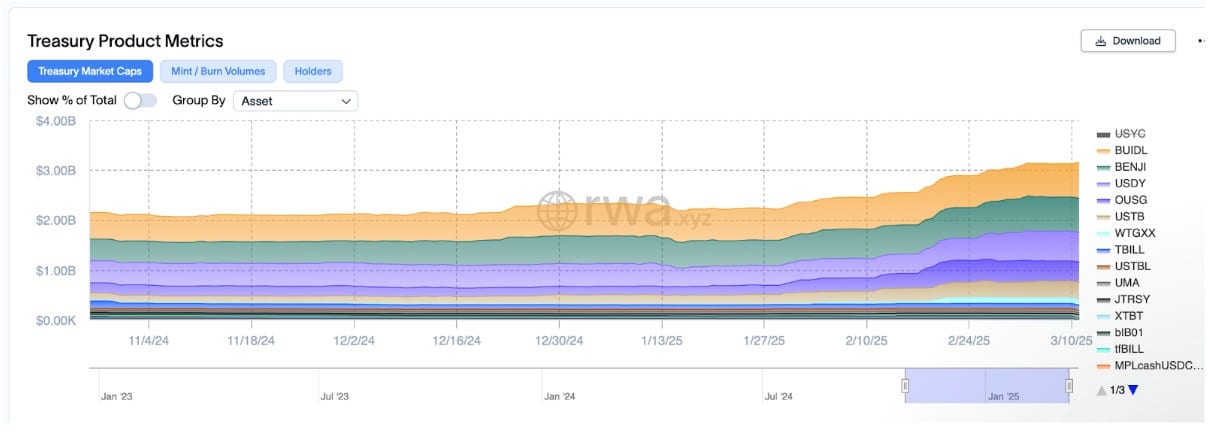

However, tokenized treasuries saw 68.3% growth over the same period, or 2.46x faster growth, to go from $2.4 billion to $4.1 billion.

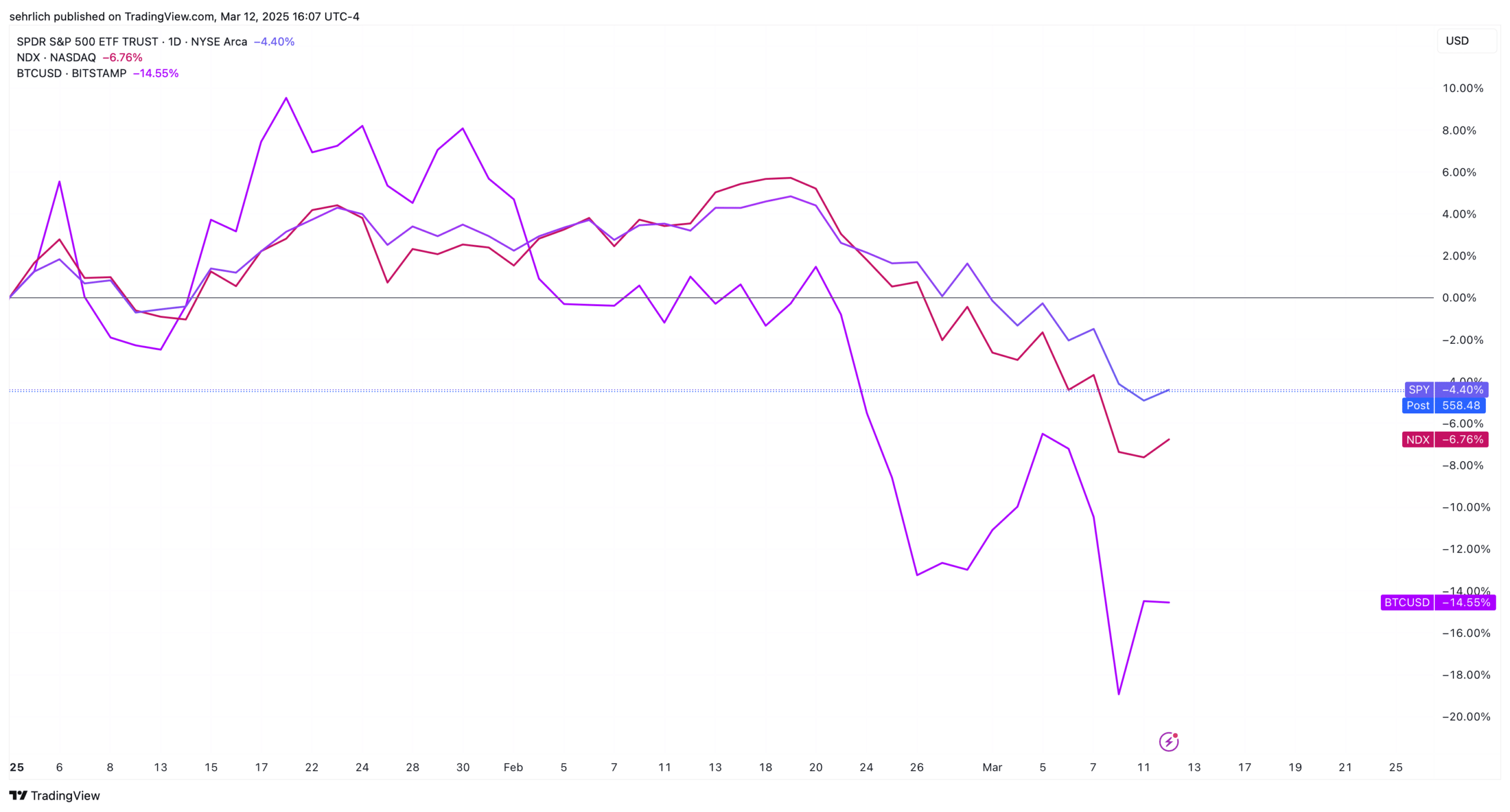

The trend is even more striking when looking at the past few weeks. Analysts typically consider the market, or an index, to be in a correction when it drops at least 10% from a recent high. Both the S&P 500 and tech-heavy Nasdaq 100 started their downward trends on February 19 and entered correction territory in the past day or so. Bitcoin is down almost 30% from its late-January high.

During the period from February 19 to March 11, the stablecoin market grew from $233.81 billion to its current $234.77 billion, a paltry 0.4%. By comparison, tokenized treasuries jumped from $3.8 billion to $4.11 billion. This amounts to 8.16% growth in just a little over two weeks.

Every Penny Counts

Multiple experts tell Unchained that a major reason for this growth in tokenized treasuries is that traders are under pressure in this economy to stretch out every gain. Tokenized treasuries are paying out an average of 4.27% annually to their holders. That may seem like a rounding error in crypto, but in this uncertain environment it suddenly becomes material, especially for sophisticated traders.

“We should expect those who post stablecoin collateral as the primary users of tokenized treasuries in order to earn yield on the collateral they are posting,” says a spokesperson for USDC issuer Circle, which recently bought $912 million tokenized treasury issuer Hashnote. One trader who wished to remain anonymous put things more succinctly: “Why use something that doesn’t give you yield when you can earn extra on top of it? It’s just putting your collateral order to work.”

FalconX, a prime brokerage, has been accepting tokenized money market funds like BlackRock’s BUIDL and Superstate’s USTB as collateral for nearly a year. Recently, the firm also began accepting Jito Staked Solana (JitoSOL) as collateral for certain trades.

“I expect the industry will continue in this direction, enabling investors to maximize asset efficiency,” said Matthew Sheffield, FalconX’s senior vice president of trading.

What’s in Your Token?

There may be more at play here. Despite their name, stablecoins have historically suffered periods of instability. Tether has been plagued by so much fear, uncertainty, and doubt (FUD) that there is a nickname for people who claim the issuer lacks the collateral to back its massive product, a “Tether Truther”. However, Tether has never failed to meet a redemption.

USDC was marketed as the antidote to USDT FUD, but even it hit some snags. In March 2023 USDC de-pegged from its price of $1.00 all the way down to $0.87 when it was revealed that the company placed $3.3 billion in unsecured collateral in troubled Silicon Valley Bank. The federal government ultimately stepped in and guaranteed all SVB deposits above the posted $250,000 FDIC limit, but investors were scarred.

During those perilous days investors learned a couple of lessons. It can be hard to know the exact makeup of a stablecoin’s collateral. Second, if you want to convert tokens back to the underlying collateral outside of normal banking hours you might be out of luck.

According to Sandy Kaul, Senior Vice President at asset manager Franklin Templeton and head of its digital assets division, tokenized treasuries are the answer.

“Yes, stablecoins can move all around the ecosystem, but they can’t be taken off-chain and go back into fiat during periods where there’s no banking hours open,” she said. Tokenized treasuries, she said, offer “more certainty about moving from an unregulated into a regulated entity.” In the event of a market calamity, Kaul said, “there’s a chance that the stablecoin might de-peg. If I can move out of that stablecoin into a US treasury, at least I know that the US treasury is a regulated vehicle [and] will not dramatically change in value overnight.”

A Tokenized Future?

It seems clear that the industry has crossed the Rubicon and tokenized treasuries will be here to stay. But the pace of growth will depend on a few factors.

One significant reason for the massive surge in these products in recent months was an October decision by Deribit, the world’s largest crypto derivatives provider, to accept Hashnote’s USYC as collateral for margin trades on the platform. The timing was extremely serendipitous, as it caught the late 2024 bitcoin wave early. On October 9, the day of the announcement, bitcoin was worth $60,370. By Trump’s inauguration it had surged 76% to top $106,000.

A lot of these traders took advantage of the basis trade, which is essentially a way to make free money by buying spot bitcoin and then selling a futures contract at a higher price. It is an extremely profitable strategy during bullish periods.

“The basis trade is obviously one of the most popular trades right now, and it’s because tradfi has basically found an above market yield opportunity that exceeds the normal 15 to 25 [basis points] that a money market manager is essentially always fighting for to outperform,” says the anonymous trader. “You can currently earn 8% on the cash and carry trade roughly, so when you see it being used in leverage situations, you’re going to earn yield on your collateral.”

The extent of this surge is obvious in the below chart, where USYC went from virtually nothing to over $1 billion in AUM.

But it would be a mistake to attribute all of the growth in tokenized treasuries to USYC. Excluding that token, the rest of the tokenized treasury market grew by 17% since February 19th. Since election day, the tokenized treasury market excluding USYC has jumped 51.68% from $2.08 billion to $3.155 billion.

This particular trade may fall out of favor in the short term given the market correction, but it should regain popularity once a new bullish cycle hits.

In the meantime tokenized treasuries could also continue to gain favor among traders who want to remain at the ready to jump on market opportunities. “It’s like any equity trader who moves from stocks into money markets,” said Steve Sosnick, chief strategist at Wall Street colossus Interactive Brokers. “It’s the same basic motivation.”